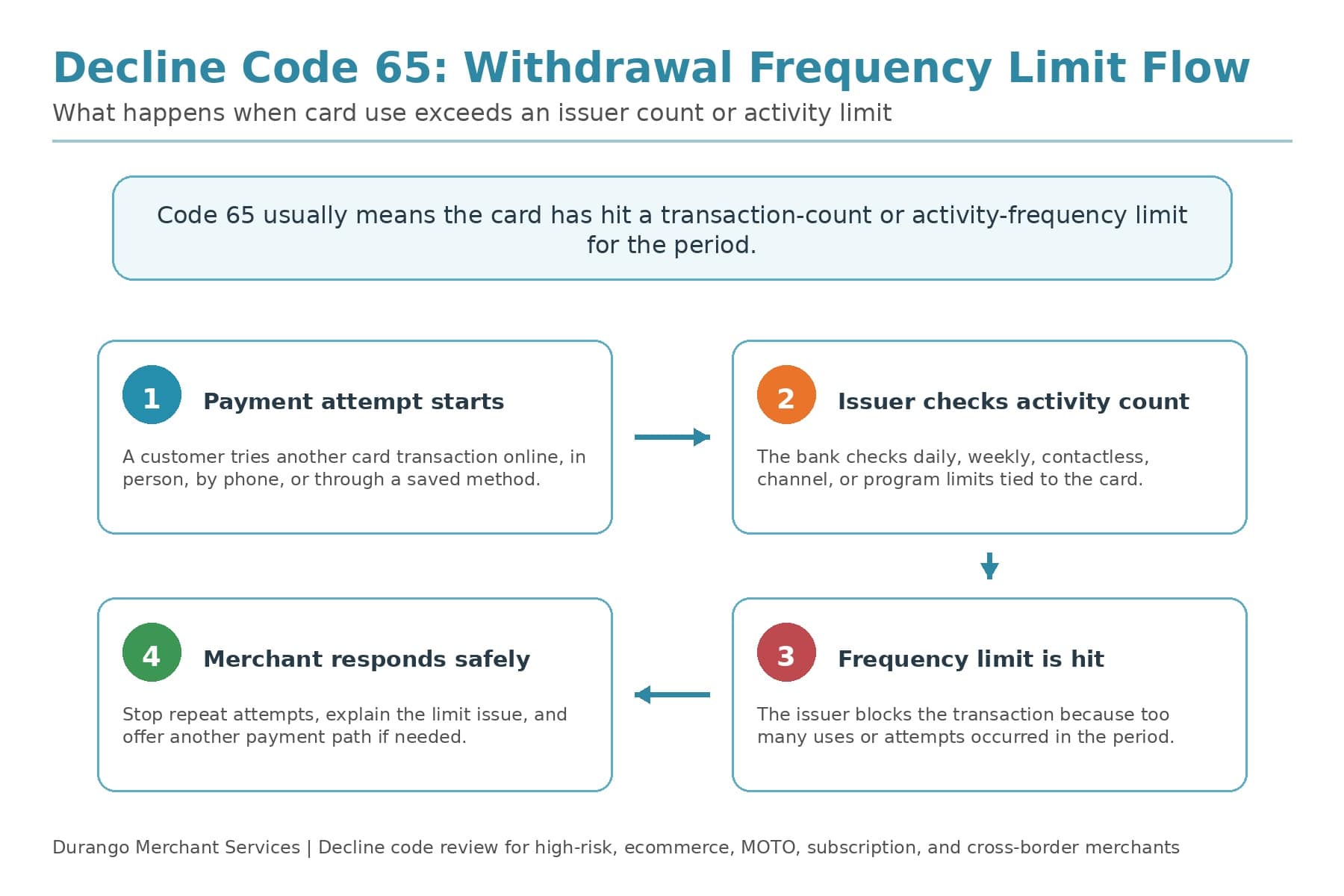

What Does Code 65: Exceeds Withdrawal Frequency Limit Mean?

The decline code 65, indicating “Exceeds withdrawal limit,” means that the transaction being attempted exceeds the withdrawal or spending limit set for the credit card. This could be a daily, weekly, or transaction-specific limit imposed by the credit card issuer to prevent overspending or fraud. When this code appears, the cardholder has likely reached or surpassed the maximum amount they are authorized to spend or withdraw within a certain period, and the transaction is automatically declined to protect the account.

Key Takeaways

- Code 65 usually means a transaction-count or activity-frequency limit was reached.

- It is different from Code 61, which is more about amount limits.

- It is also different from insufficient funds.

- Do not keep retrying the same card.

- If Code 65 repeats often, review channels, card types, contactless counters, and gateway patterns.

Code 65 is not the payment system saying, “This customer has no money.” It is more like a referee calling a usage limit. The card has crossed a frequency line set by the issuer, card program, or account controls.

For merchants, the best move is to protect the sale without creating a string of repeat declines.

What Code 65 Means in Plain English

Card issuers do more than check whether an account has money. They also enforce usage rules. Those rules may limit how many transactions can happen in a day, how often a card can be used, how many contactless payments can occur before PIN or stronger authentication is required, or how much activity a certain card program allows.

When Code 65 appears, the issuer is usually saying the card has reached a frequency or activity limit.

That makes Code 65 different from Code 61, which is more about exceeding an amount limit.

Common Reasons Code 65 Happens

Code 65 can be caused by normal card controls, fraud controls, contactless rules, or card-program limits.

- Too many card transactions in a short period

- Daily or weekly transaction-count limit reached

- Contactless counter or tap-to-pay limit reached

- Issuer requires PIN, 3D Secure, or stronger authentication

- Card-program controls limit the number of uses

- Repeated failed attempts push the card past an activity threshold

- Business, debit, prepaid, or benefits card usage rules are triggered

- Cross-border, MOTO, ecommerce, or subscription activity looks outside the normal pattern

One Code 65 decline may be a customer-card issue. A cluster may show that a channel, issuer group, or payment route is creating avoidable friction.

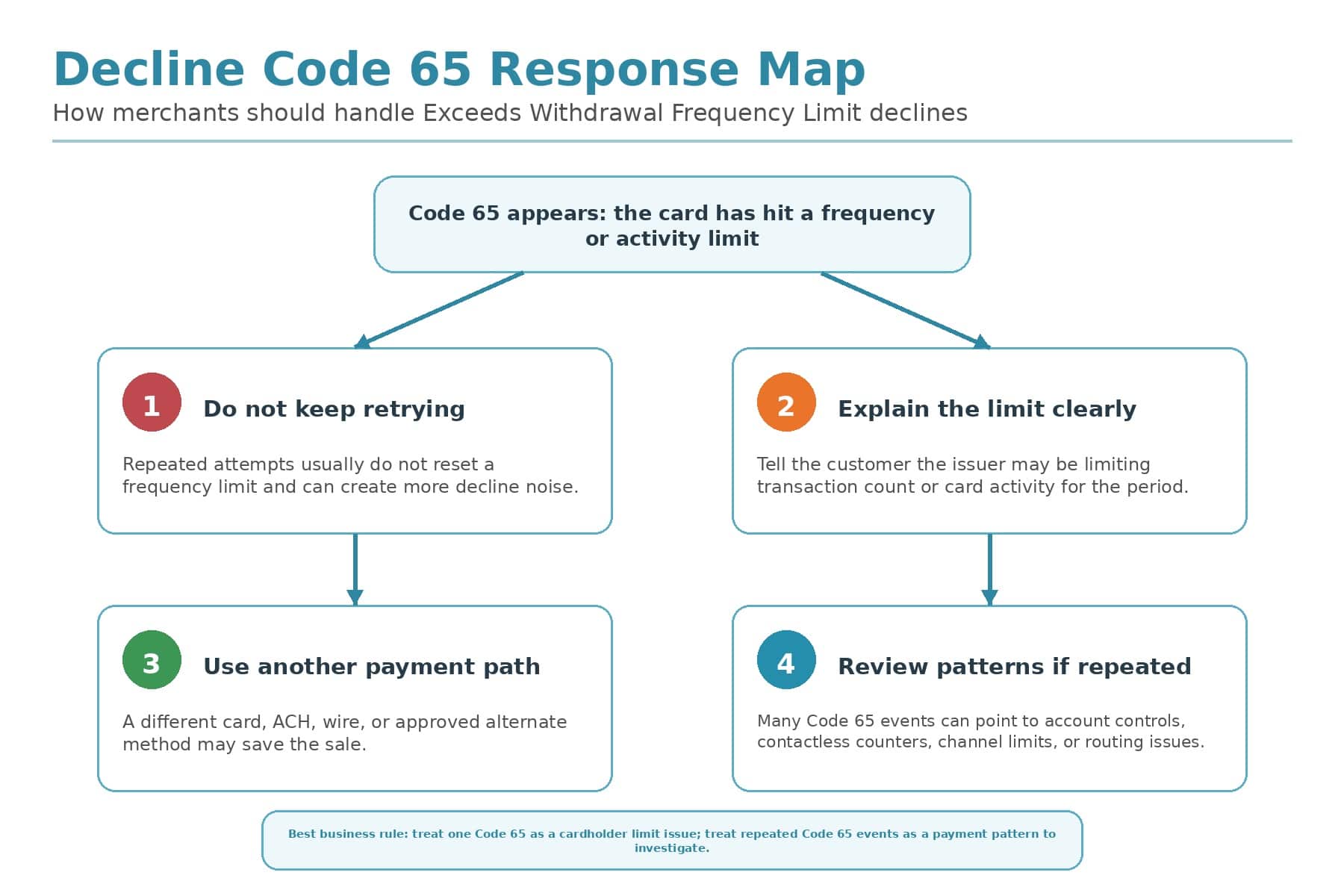

What the Merchant Should Do

Treat Code 65 as a limit signal, not a mystery decline.

- Do not keep retrying. Repeated attempts usually do not reset a frequency limit.

- Explain it simply. Tell the customer the bank may be limiting card activity for the period.

- Ask the customer to contact the issuer. The bank can confirm the limit and whether it can be reset or raised.

- Offer another payment method. A different card, ACH, wire, or approved alternate option may save the sale.

- For ecommerce, check authentication. If the issue relates to SCA, PIN, or 3D Secure, route the customer through the right authentication step.

- Track repeated events. Look for patterns by issuer, card type, country, channel, terminal, or gateway.

What Not To Do

Code 65 creates frustration because the card may look perfectly usable. That is when a poor response can create more declines.

- Do not assume the customer lacks funds.

- Do not keep running the same card over and over.

- Do not treat Code 65 the same as Code 51 or Code 61.

- Do not accuse the customer of fraud.

- Do not ignore repeated declines from the same channel or issuer group.

- Do not bypass required authentication just to force the sale.

The goal is not just to get one payment through. The goal is to preserve approval rates, protect the customer experience, and avoid unnecessary processor risk signals.

When Merchants Should Look Deeper

A single Code 65 decline may only mean the cardholder hit a temporary limit. Repeated Code 65 declines deserve a closer look.

- A spike appears after adding contactless, mobile, or saved-card payments

- Subscription rebills trigger more Code 65 declines than new sales

- MOTO or manually keyed payments show the highest failure rate

- Cross-border cards decline more often than domestic cards

- One issuer, country, card brand, terminal, or gateway route stands out

- Customers report that their card works elsewhere

- Failed attempts happen in bursts from the same device, IP address, or account

- Approval rates drop while traffic and demand stay steady

Those patterns can point to issuer controls, authentication gaps, contactless counters, or retry logic.

How Durango Merchant Services Can Help

Durango Merchant Services helps merchants read decline codes as business signals, not just short technical messages.

For high-risk, ecommerce, MOTO, subscription, travel, large-ticket, and cross-border merchants, Code 65 can expose friction in authentication, retry logic, payment methods, or processor setup.

If Code 65 keeps appearing in your reports, contact Durango Merchant Services. We can review the pattern, protect legitimate sales, and build a cleaner payment path.

FAQs For Decline Code 65

It means the card has exceeded a withdrawal frequency, transaction-count, or activity limit. The issuer is blocking more usage until the limit resets or the customer contacts the bank.

No. Code 65 is a frequency or activity-limit issue. Insufficient funds is a different decline condition tied to available balance.

Do not keep retrying the same card. The limit may need time to reset, or the customer may need to contact the issuer.

Investigate when Code 65 appears repeatedly across customers, card brands, countries, channels, terminals, or gateway routes.